I wrote my first blog post in a while last week, and it felt quite cathartic to unload a lot of the frustration I have with the evolution of online payments over the last decade. The post got a lot of attention (front page of Hacker News for a few hours) and directed thousands of new users to our website where many got onto our waitlist. (If you were one of them, thank you.)

As a follow up I wanted to answer some of the questions that came up in response to my rant about online card payments and the duopoly of Apple and Google taking over the online payments ecosystem with their digital wallets, largely unchallenged.

It’s easy to criticise, it’s harder to come up with workable solutions to the problems you’ve identified, and even harder to build those solutions as products and turn them into a viable business. This is the path we’ve chosen at Fynbos and we’re excited by the challenge.

Our thesis is simple; the future of digital payments is going to centre on digital wallets.

Once wallets have abstracted away the complexity of the various payment methods used by people around the world, there will only be one payment method used online, pay-by-wallet, and the underlying payment instruments and rails used to complete the actual transfer of funds will be immaterial.

We see this happening already with Apple Pay and Google Pay where the user experience of using these wallets feels like magic in comparison with manual card data entry and yet the actual payment is being done with a card (neatly tucked away in the wallet and tokenised for the purpose of the transaction).

Wallets exploiting their superior user experience in order to gain market share is specific to card-centric ecosystems like the US. Payments are very different around the world. In fact, some commentators on my last blog post suggested I was taking a very US-centric view in that post, and they are not wrong. But our thesis at Fynbos extends to the rest of the world too, where digital wallets sit in front of other payment methods, often specific to that region.

Take, for example, the success of Google Pay in India where payments run on the UPI rails and Google are responsible for 34% of the usage in 2022. Their only real competitor is PhonePe, another digital wallet, but one that has no offering outside of India.

Similar instant payment systems that offer alternative rails to cards for e-commerce are springing up all over the world (see PIX in Brazil, FasterPayments in the UK, NETS/PayNow in Singapore etc.) and it’s no surprise that in each case there are digital wallets clambering to capture the market of new users. Google went as far as to write a white paper advising national payment system architects on how to design their instant payment systems to accommodate “over the top” players or “payment initiation service providers” like themselves (effectively giving them an edge over incumbents like banks in this role).

The fact that the payment instrument for card payments (the PAN) has also been the primary means for users to access the card payments rails is, as we would say in the software engineering world, a leaky abstraction. Wallets create a clean abstraction layer between users, their accounts, the payment rails their accounts are connected to and the counter-parties they transact with. Users don’t care about how the money moves, they care about the experience. Key to the experience is how much they trust “the system”, and for most users this is manifested for them as the interface they use (their wallet).

But, while the Internet has been making the world smaller for decades, all of the new instant payment innovations are generally regional. Cross-border is where the international card networks still have an edge but the question is, for how long? It’s not hard to imagine Google Pay enabling a payment from a US credit card to an Indian merchant where neither the consumer nor the merchant even know that the payment is completed first via the card networks and then UPI.

How then does PhonePe extend their reach outside India?

How does the Brazilian creator, that usually receives instant payments via PIX, sell to the Indian consumer, that usually pays for everything online using their PhonePe wallet?

Forget about connecting the payment rails for a second. This is a known problem, and is being rapidly resolved by both public and private initiatives. Look no further than the Interledger project, Nexus from the Bank for International Settlements, the various initiatives at SWIFT such as GPI+, or fintechs using cryptocurrency like Ripple and Circle.

What all of these systems assume is that somebody else will build the user facing products on top of their cross-border rails, the wallets.

In most cases, wallets use an alias (email address, mobile number, national identity number, or similar) to handle discovery in the person-to-person (P2P) use case. The sender types in the alias of the receiver to kick off the flow and their wallet looks up the receiver in a directory. Except there is a unique directory in each country/region so this whole cross-border thing just got a lot harder. If only there was a global directory of names that mapped to service addresses… like the one we use every day for email and browsing the Web.

The e-commerce (consumer-to-business or C2B) use case is even more of a mess. The way you initiate wallet payments today is by picking your wallet’s button on the checkout screen. Fine if there are only 2 or 3 choices in your country but imagine a checkout page with the logo of every digital wallet in the world displayed for you to choose how to pay. Nascar problem anyone?

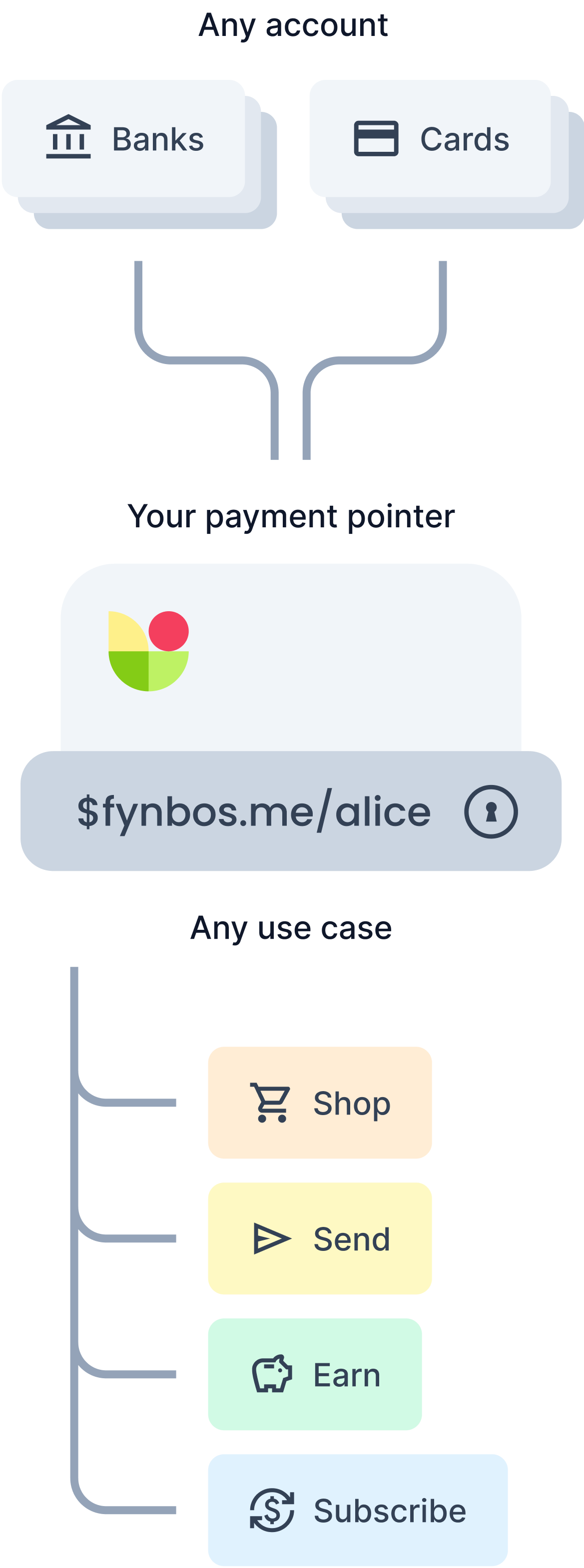

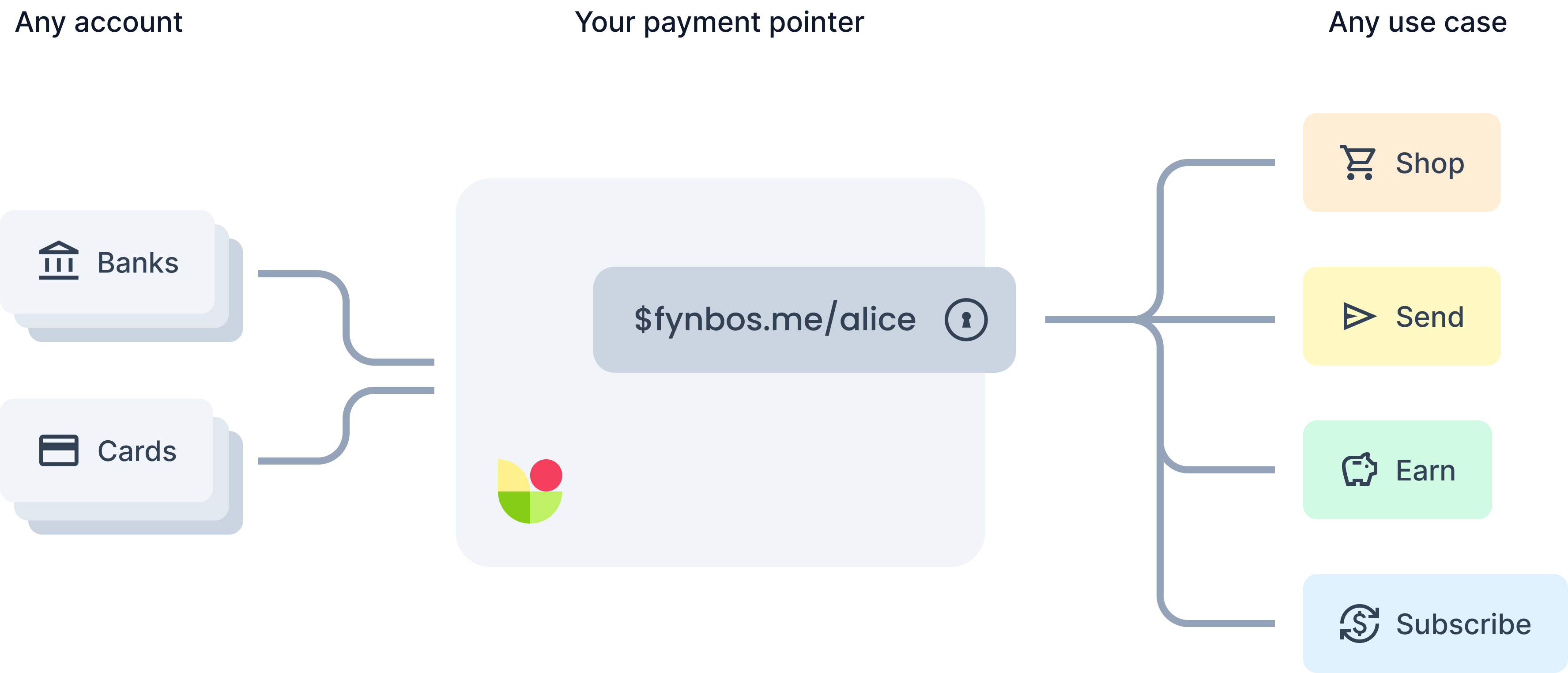

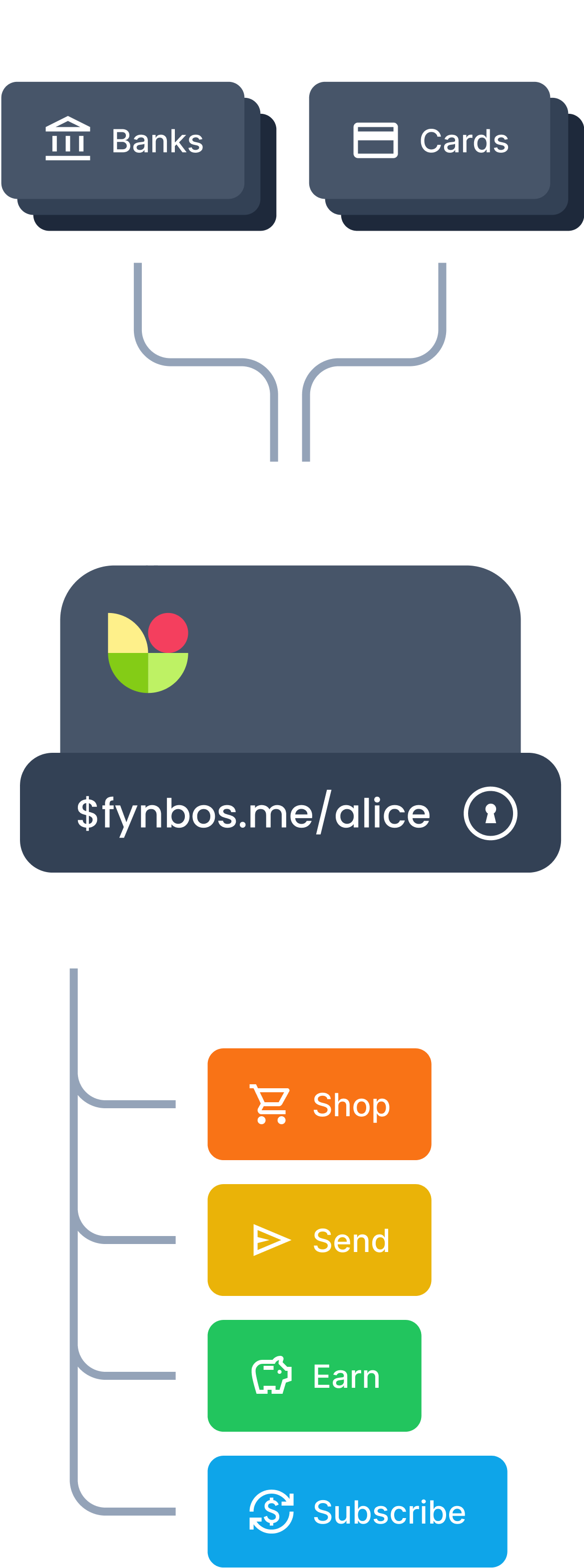

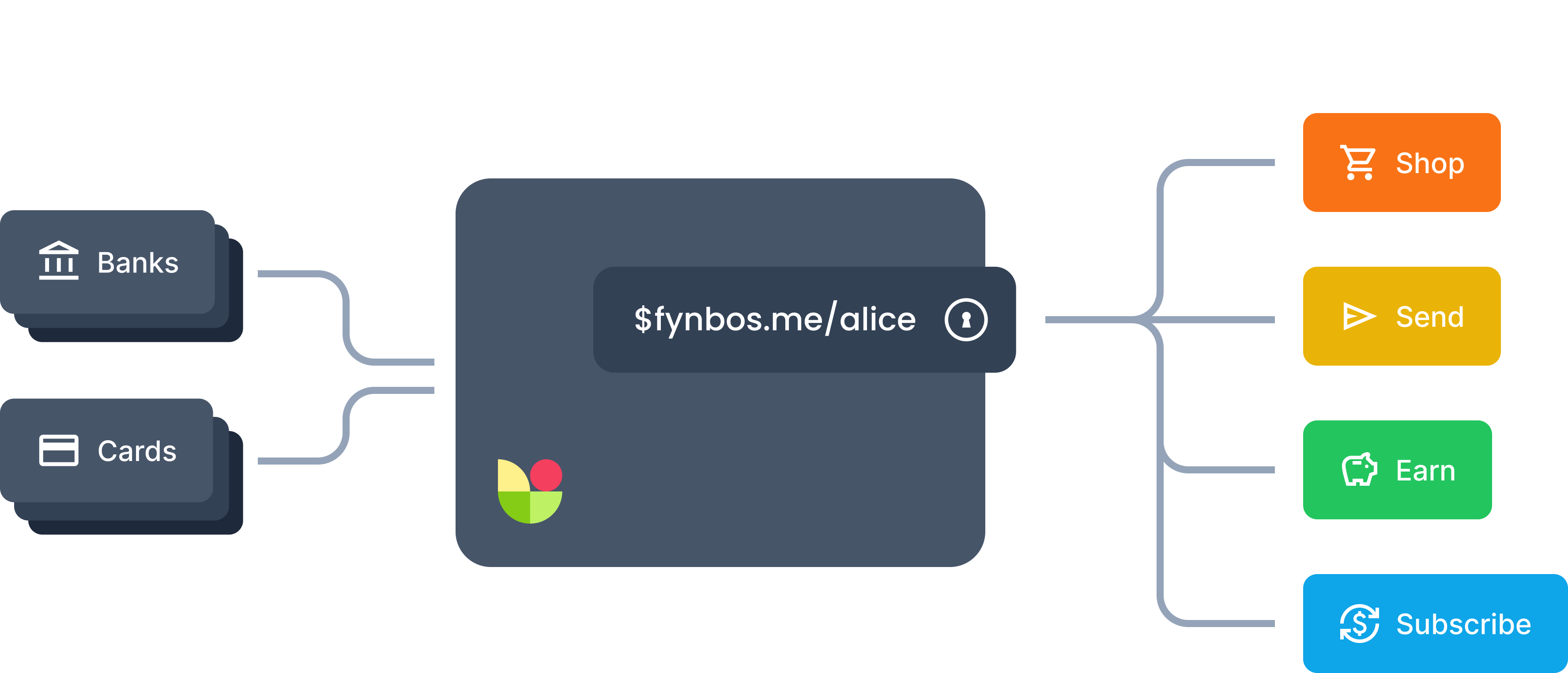

The solution we’re building at Fynbos is based on an open standard called payment pointers. It’s like an email address but for your digital wallet. Payment pointers are just URLs but we’ve made them easy to recognise as a payment-related alias and easy to remember and transcribe. Here’s an example:

$fynbos.me/adrian

Anybody in the world will be able to use that payment pointer to send a payment to my Fynbos wallet and I can use it to checkout online, no matter where in the world the store I’m shopping at is based. Well, that’s the plan, we’re still in private beta. Here’s a video of the UX we envision for the future of e-commerce to whet your appetite:

There’s a lot more to tell about payment pointers and the incredible use cases that are unlocked by a digital wallet that is addressable via APIs at a public URL. Stay tuned for my next blog post to start unpacking these ideas and in the mean time get on our waitlist.